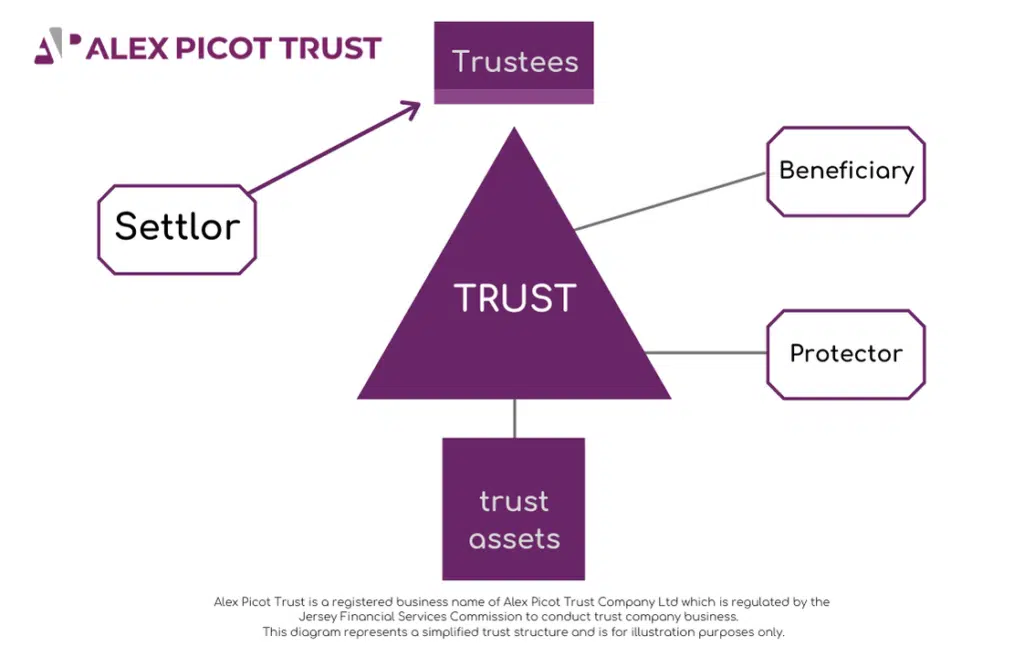

Settlor-taxed non-UK resident trusts – income tax and capital gains tax

In the last part in our series on offshore trusts we considered rules for establishing trust residence. Once it is established that a trust is non-UK resident, our thought turns to how it will be taxed in the UK. A key consideration is whether the settlor retains an interest in the trust, i.e. whether it is settlor-interested. In this article we consider when a trust is settlor-interested for UK income tax and capital gains tax purposes and the tax implications of this.

This is part 3 of our Offshore Trusts blog series, written by our Senior Tax Manager Lawrence Adair. Read part one here: ‘All you need to know about Offshore Trusts’ . Read part two here: ‘Residence Positions and Offshore Trusts’

The definition of settlor-interested for capital gains tax is wider than that for income tax. Each tax is considered separately below, starting with income tax.

Income tax – definition of settlor-interested

For income tax, a settlor is broadly treated as having an interest in a trust if trust assets are or may become payable to, or applicable for the benefit of, the settlor or his spouse / civil partner. For clarity on the position, trust deeds often explicitly include or exclude the settlor and their spouse / civil partner.

Income tax on settlor-interested trusts – UK income

UK income received by a settlor-interested offshore trust is initially taxable on the trust at up to 45%. This is depending on the type of trust and income source. However, the income is also taxable on the settlor at up to 45% including income from underlying offshore companies, where broadly there was a UK tax avoidance motive in setting up the trust structure.

To avoid double taxation the settlor gets credit for the income tax paid by the trust. In addition, if the settlor is required to pay additional tax on trust income then the additional liability can be recovered from trust. Conversely, if the settlor receives a tax refund this must be paid over to the trust.

A settlor can also be assessable on trust income where their minor child can benefit. This is not a general assessment on them but only where their child receives a distribution from the trust.

Income tax on settlor-interested trusts – non-UK income

Unlike UK income, non-UK income received by a settlor-interested offshore trust is not taxable on the trust. But the default position is that it is still taxable on the settlor at up to 45%. Again, this includes income from underlying offshore companies. Where, broadly there was a UK tax avoidance motive in setting up the trust.

However, settlor-interested rules are ‘switched off’ for certain trusts created by non-UK domicilairies. If the non-UK income is ‘protected foreign source income’. In which case, the income is only assessable when it is distributed. Furthermore, the settlor will only be assessable to the extent that they receive a distribution. (Except for exceptions for distributions to a spouse or minor child who are not immediately assessable to UK tax on the distribution.)

Conditions

Several conditions apply for income to be protected foreign source income, mainly focused on the settlor’s domicile. They must have been non-UK domiciled and not deemed domiciled when the trust was created. And not have become UK domiciled or a ‘formerly domiciled resident’. (Broadly born in the UK with a UK domicile at birth and has returned to the UK.)

Tainting

Also crucial is that the trust must not become ‘tainted’ so care is needed to avoid this. Tainting occurs when the settlor provides property or income, for the purposes of the trust, at a time when they are UK domiciled or deemed domiciled. This includes property provided directly or indirectly. Tainting occurs from the first tax year in which property is provided. An obvious example of tainting is where further assets are added by the settlor. Less obvious examples of tainting include settlor loans where the interest charged is less than HMRC’s official interest rate.

A settlor tax charge is subject to a remittance basis claim where the distribution is not remitted to the UK.

Protected Trust

A protected trust will be particularly useful where a settlor can no longer claim the remittance basis. And trust distributions can be restricted to being made only when required. They can also allow avoiding the need to pay the remittance basis charge where the settlor’s only non-UK income is protected trust distributions brought to the UK.

As well as income distributions, it is possible for distributions which are capital in nature, to be matched to protected foreign source income. Where, broadly there was a UK tax avoidance motive in setting up the trust.

Capital gains tax – definition of settlor-interested

There is a wider, more complex, definition of settlor-interested for capital gains tax purposes. As for income tax it includes where the settlor or spouse /civil partner can benefit. It also includes potential or separated spouses, children, grandchildren and companies controlled by any of these individuals. However, for a trust to be settlor-interested for a particular tax year, a defined person must be able to benefit, and the settlor must be both UK resident and UK domiciled.

For the domicile requirement, there are protections to ignore deemed domiciles. These mirror the income tax protections outlined above for foreign income, including tainting of the trust. If the protections are met, the trust is not settlor-interested for capital gains tax.

Capital gains tax – assessment of gains on settlor

An offshore trust is not liable to capital gains tax except for gains on UK property interests. Instead non-UK property gains are either assessable on the settlor or beneficiaries with those realised by a non-protected settlor-interested trust assessable on the settlor at up to 28% depending on the type of gain. This includes gains from underlying offshore companies, where broadly there was a UK capital gains tax or corporation tax avoidance motive in setting up the trust.

To avoid double taxation the settlor can recover any capital gains tax paid from the trust.

Trust capital losses, however, can only be set against settlor-interested trust gains of the same or future tax year. They cannot be set against the settlor’s personal gains.

3 most important points to take away

The settlor or his family benefitting from a trust can make it settlor-interested so that the settlor is assessed on trust income and gains as they arise.

Non-UK domiciled settlors can be protected from settlor-interested rules so that foreign income or gains assessed on them are limited to distributions.

For non-UK domiciled settlors to benefit from settlor-interested trust protections it is important that the trust does not become tainted.

Written by Lawrence Adair